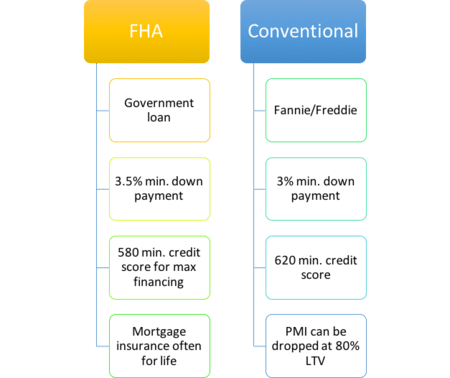

𝗧𝗵𝗲 𝗶𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝘁𝗵𝗶𝗻𝗴 for you to know is that conventional loans have many benefits, including:

Down payments as low as 3%

No upfront mortgage insurance premium

Monthly mortgage insurance that automatically falls off once the home has been paid down to 78% of the home’s value

The ability to choose between an adjustable-rate or fixed-rate mortgage with different term lengths

Use on different property types, including primary residences, second homes, and investment properties

✔ Maximum Loan Limits set each year.

✔ PMI based on credit score and equity position

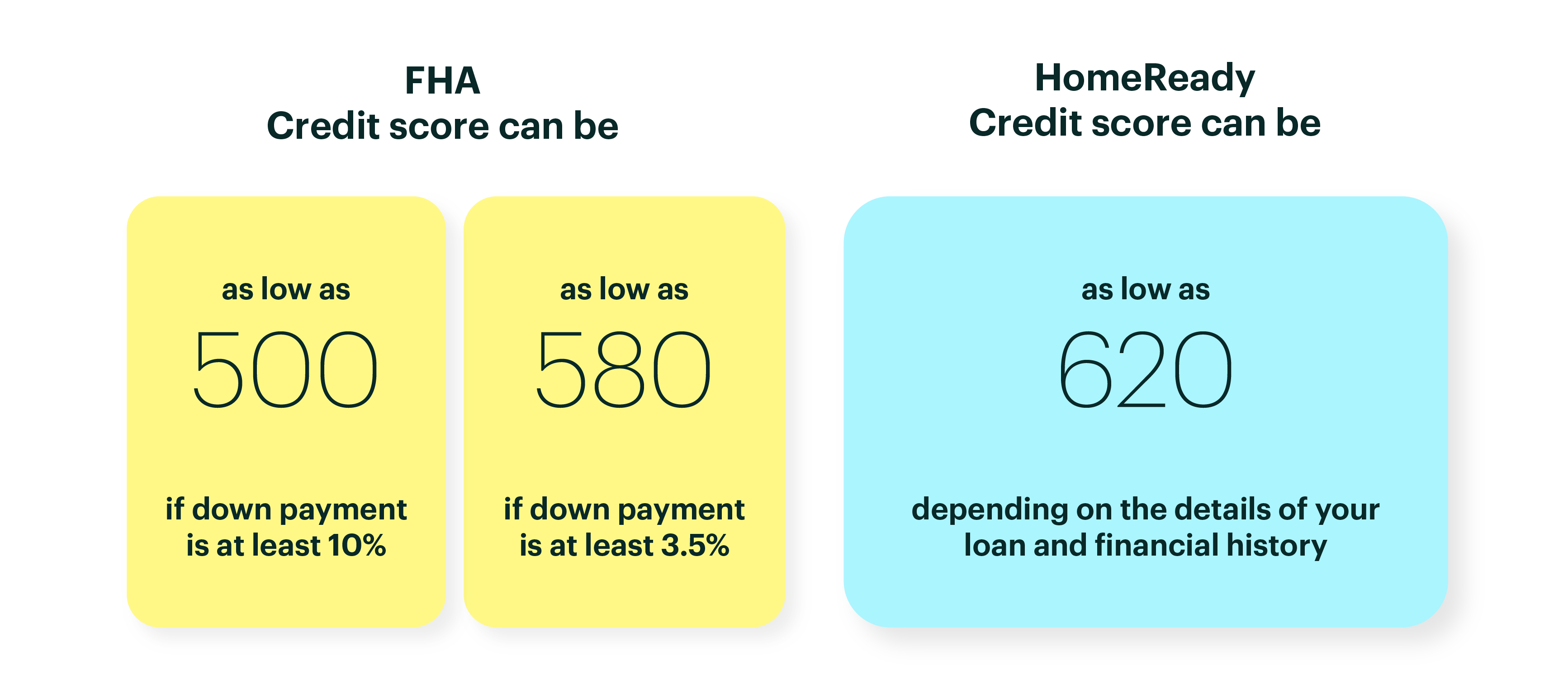

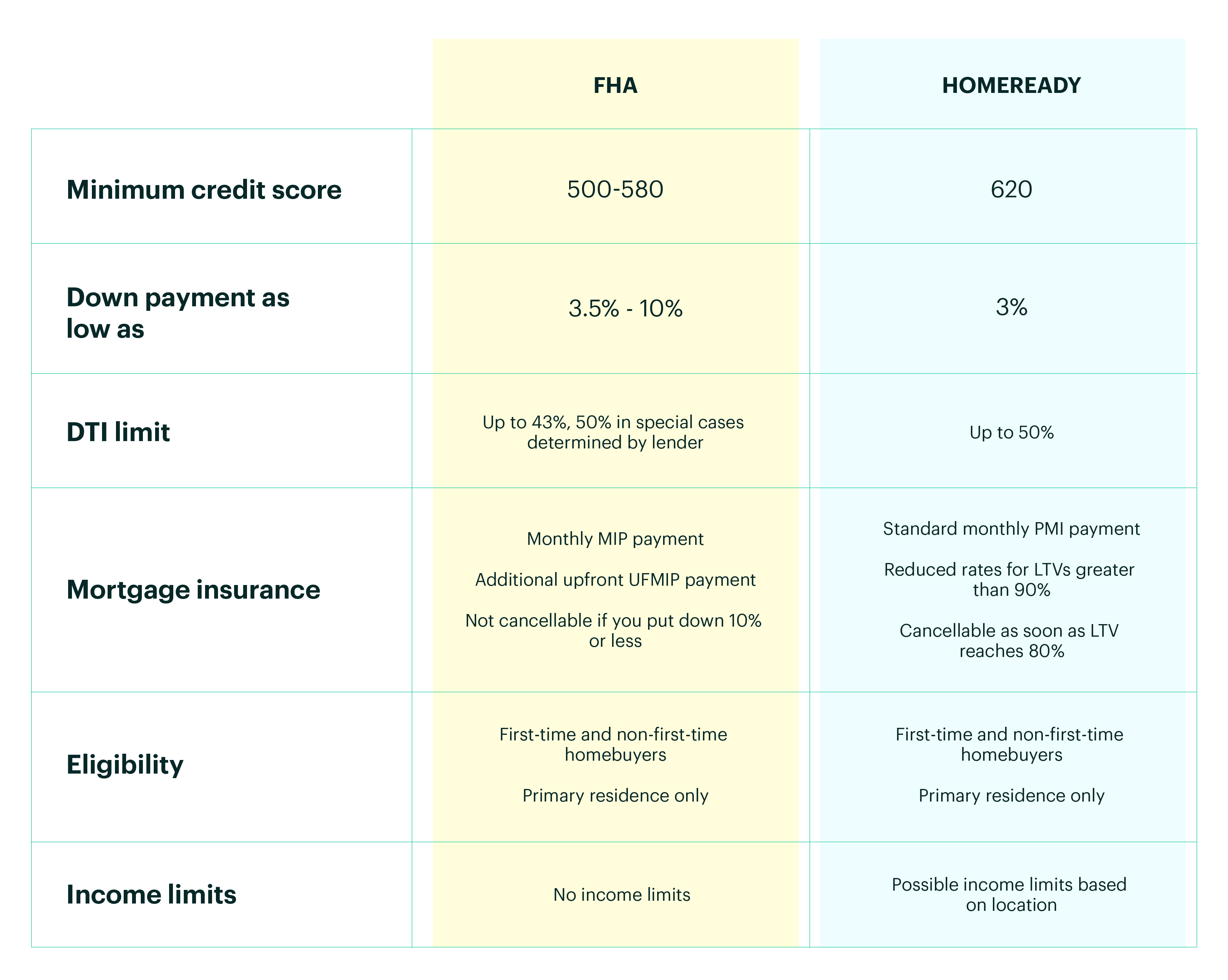

Kentucky Fannie Mae Loans versus Kentucky FHA Loans

|

|

Non Occupant Co-Borrower for Fannie Mae and FHA Loans.

The differences below: |

Kentucky Fannie Mae Loans - Allowed on all Purchases up to 95% LTV

- Allowed on all Refinances including Cash out

- Does not have to be a Family Member

Kentucky FHA Loans - Limited to 75% LTV. LTV can be increased to max 96.5% LTV provided:

- Non occupying borrower is not the seller in the transaction

- Property is not a 2-4 unit property

- Has to be a family member

- Not allowed on Cash out Refinances

- Non Occupant Co Borrowers must either be United State Citizens or have a Principal Residence in the United States.

|

|

Non arms Length / Identity of Interest for FHA and Fannie Mae Loans In KY |

Fannie Mae Loans(non arms length) - Underwriter must confirm transaction is not a bail out

- Gift of Equity is allowed

- No additional restrictions apply

FHA loans (Identity of Interest) - Gift of Equity is allowed

- LTV limited to 85% unless

- Purchase is the principle residence of another Family Member

- Borrower has been a tenant in property for 6 months predating the sales contract. A lease or other written evidence is needed to verify occupancy

- Borrower is an employee of the Builder of the property

- If a Family Member is providing secondary financing for the transaction, additional guidelines apply. See HUD 4000.1 II.A.4.(3) for additional guidelines.

Joel Lobb

Mortgage Loan OfficerIndividual NMLS ID #57916

American Mortgage Solutions, Inc.

Text/call: 502-905-3708

|

|