As a Kentucky First time home buyer, there are questions that arise about how to qualify for a mortgage loan and what type of loan programs are available to first time buyers. Below I have addressed some of the more common questions that may arise.

∘ What kind of credit score do I need to qualify for different first-time home buyer loans in Kentucky?

Answer. Most lenders will want a middle credit score of 620 to 640 for KY First Time Home Buyers looking to go no money down. The two most used no money down home loans in Kentucky being USDA Rural Housing and KHC with their down payment assistance will want a 620 to 640 middle score on their programs.

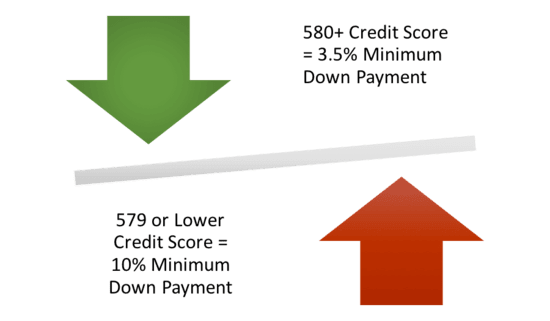

If you have access to 3.5% down payment, you can go FHA and secure a 30-year fixed rate mortgage with some lenders with a 580-credit score. Even though FHA on paper says they will go down to 500 credit score with at least 10% down payment, you will find it hard to get the loan approved because lenders will create overlays to protect their interest and maintain a good standing with FHA and HUD.

Another popular no money down loan is VA. Most VA lenders will want a 580 middle credit score but like FHA, VA on paper says they will go down to a 500 score, but good luck finding a lender for that scenario.

A lot of times if your scores are in the high 500’s or low 600’s range, we can do a rapid rescore and get your scores improved within 30 days.

∘ Does it cost anything to get pre-approved for a mortgage loan?

Answer: Most lenders will not charge you a fee to get pre-approved, but some lenders may want you to pay for the credit report fee upfront. Typically costs for a tri-merge credit report for a single borrower runs about $50 or less. Maybe higher if more borrowers are included on the loan application.

∘ How long does it take to get approved for a mortgage loan in Kentucky?

Answer: Typically, if you have all your income and asset documents together and submit to the lender, they typically can get you a pre-approval through the Automated Underwriting Systems within 24 hours. They will review credit, income and assets and run it through the different AUS (Automated Underwriting Systems) for the template for your loan pre-approval. Fannie Mae uses DU, or Desktop Underwriting, FHA and VA also use DU, and USDA uses a automated system called GUS. GUS stands for the Guaranteed Underwriting System.

If you get an Automated Approval, loan officers will use this for your pre-approval. If you have a bad credit history, high debt to income ratios, or lack of down payment, the AUS will sometimes refer the loan to a manual underwrite, which could result in a longer turn time for your loan pre-approval answer

∘ Are there any special programs in Kentucky that help with down payment or no money down loans for KY First Time Home Buyers?

Answer: There are some programs available to KY First Time Home Buyers that offer zero down financing: KHC, USDA, VA, Fannie Mae Home Possible and HomePath, HUD $100 down and City Grants are all available to Kentucky First Time Home buyers if you qualify for them. Ask your loan officer about these programs

∘ When can I lock in my interest rate to protect it from going up when I buy my first home?

Answer: You typically can lock in your mortgage rate and protect it from going up once you have a home picked-out and under contract. You can usually lock in your mortgage rate for free for 90 days, and if you need more time, you can extend the lock in rate for a fee to the lender in case the home buying process is taking a longer time. The longer the term you lock the rate in the future, the higher the costs because the lender is taking a risk on rates in the future. Interest rates are kind of like gas prices, they change daily

∘ How much money do I need to pay to close the loan?

Answer: Depending on which loan program you choose the outlay to close the loan can vary. Typically, you will need to budget for the following to buy a home: good faith deposit, usually less than $500 which holds the home for you while you close the loan. You get this back at closing; Appraisal fee is required to be paid to lender before closing.

There are also lender costs for title insurance, title exam, closing fee, and underwriting fees that will be incurred at closing too. You can negotiate the seller to pay for these fees in the contract, or sometimes the lender can pay for this with a lender credit. The lender has to issue a breakdown of the fees you will incur on your loan pre-approval.

How long is my pre-approval good for on a Kentucky Mortgage Loan?

Answer: Most lenders will honor your loan pre-approval for 60 days. After that, they will have to re-run your credit report and ask for updated pay stubs, bank statements, to make sure your credit quality and income and assets has not changed from the initial loan pre-approval.

How much money do I have to make to qualify for a mortgage loan in Kentucky?

Answer: The general rule for most FHA, VA, KHC, USDA and Fannie Mae loans is that we run your loan application through the Automated Underwriting systems, and it will tell us your max loan qualifying ratios.

There are two ratios that matter when you qualify for a mortgage loan. The front-end ratio is the new house payment divided by your gross monthly income. The back-end ratio is the new house payment added to your current monthly bills on the credit report, to include child support obligations and 401k loans.

Car insurance, cell phone bills, utilities bills does not factor into your qualifying rations.

If the loan gets a refer on the initial desktop underwriting findings, then most programs will default to a front end ratio of 31% and a back-end ratio of 43% for most government agency loans that get a refer. You then take the lowest payment to qualify based on the front-end and back-end ratio.

So for example, let’s say you make $3000 a month and you have $400 in monthly bills you pay on the credit report. What would be your maximum qualifying house payment for a new loan?

Take the $3000 x .43%= $1290 maximum back-end ratio house payment. So take the $1290-$400= $890 max house payment you qualify for on the back-end ratio.

Then take the $3000 x .31%=$930 maximum qualifying house payment on front-end ratio.

So now you know! The max house payment you would qualify would be the $890, because it is the lowest payment of the two ratios.

There are basically 4 mortgage programs for first time home buyers in Kentucky to consider:

1. FHA LOANS IN KENTUCKY

Kentucky FHA loans are a popular choice in Kentucky first time home buyers

because they allow the least down payment of 3.5% and can use down payment assistance to meet the 3.5% down payment requirements.

The current credit score requirements center around the 580-620 score for most FHA loans in Kentucky,

Even though FHA insure a mortgage loan down to a 500 credit score or lower sometimes, it is very

difficult to find a lender that will approve the loan with scores below 580.👀

The house payment will need to be around 30% of your gross monthly income. For example, if

you gross around $3000 a month, then the maximum mortgage payment you would qualify

would be $1000 a month. If the loan comes back as an accept, the debt-to-income ratio can be

substantially higher than the 31% rule.

All FHA loans are pre-approved through an AUS, an automated underwriting system upfront

that will dictate your loan approval. The software underwriting engine looks at your credit, income, assets and figures your loan approval and will recommend an accept, refer/eligible, or refer/ineligible, or out of scope.

Most FHA investors will want a Accept on your underwriting findings to do a loan. It it comes back

referred, then there are additional conditions or overlays that could stop your loan from being approved.

2. Kentucky VA Home Loans

Kentucky VA loans require no down payment, but you must have a VA certificate of Eligibility issued by the Veterans Administration to purchase a home using your VA loan entitlement.

The current credit score that most Kentucky VA lenders want is 580-620. There can be no bankruptcies or

foreclosures in the last two years with good, reestablished credit.

The maximum debt to income ratio is 41% with a residual income of around $1000 a month after you pay all your bills. For example, if you make $4000 gross monthly, then the maximum house payment

along with your other household bills would be set at $3000 a month so as you have the $1000 residual income requirement met.

3. Kentucky USDA/Rural Housing:

Kentucky USDA loans require no down payment and are subject to income and property eligibility requirements by County.

Check Kentucky USDA Income Limits Here"----->>>>

Check Kentucky USDA Property Eligibility Limits Here--->>>>

All Kentucky Rural Housing Loans are ran through GUS, Guarantee Underwriting System, an

online to determine your loan approval The Automated Underwriting engine will come back with an Accept, Refer, or Ineligible.

Most Kentucky USDA mortgage investors want an Accept on the initial underwriting approval to do the loan or at least a 620 to 640 score to do a manual underwrite on the loan.

640 is the score that most USDA lenders want, but USDA will go down to a 581-credit score in the

guidelines but it is very difficult to get approved. If you have a score below 640 and trying to go USDA, work on getting your credit scores up first.

4. Kentucky Housing Corp Down Payment Assistance

Kentucky Housing Corporation (KHC) offers a down payment assistance program to help Kentucky First Time Home buyers buy a house with no down payment.

Guidelines for the $10,000 Down Payment Assistance Program for Kentucky Homebuyers:

Provides up to $10,000 in down payment assistance.

This assistance is offered as a second mortgage with a fixed interest rate.

Typically, the second mortgage is repaid over a 10-year term, but terms can vary.

Income Limits: Borrowers must meet certain income limits, which vary by county and household size. see link here for limits https://www.kyhousing.

org/Homeownership/Future- Homebuyers/Documents/SMP% 20Income%20Limitations.pdf Credit Score: Minimum credit score requirements apply, generally starting at 620 for government loans VA, USDA and FHA while Conventional loans require a 660 score

First-Time Homebuyer Status: While KHC primarily targets first-time homebuyers, some programs may allow repeat buyers in certain circumstances.

Homebuyer Education: Completion of a homebuyer education course may be required for conventional loan programs. Government-backed programs do not require homebuyer education courses.

Property Requirements: Must be primary residence and no second home homes or rental properties. The home must meet certain criteria, such as being a primary residence and meeting property condition standards. No subject to properties or fixer uppers or rehab houses. Kentucky properties only

Debt to Income Requirements. Front end and back end debt ratio cannot be more than 50%

Purchase price Limits $510,939 is the current purchase price limit. Changes yearly.

Joel Lobb Mortgage Loan Officer NMLS 57916

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.