Kentucky Home Buyers: What Credit Score Do You Need?

Buying a home in Kentucky? Your credit score plays a crucial role in determining which mortgage loans you qualify for and how much you’ll pay in interest rates. Understanding the minimum credit score requirements for FHA, VA, USDA, and Conventional loans can help you prepare for homeownership and secure the best loan options.

While there's no single, simple answer, this guide will break down the minimum credit score requirements for various Kentucky mortgage options, empowering you to understand where you stand and how to achieve your homeownership goals. We'll cut through the confusion and give you the straight facts!

Why Your Credit Score Matters: More Than Just a Number

Think of your credit score as your financial reputation. Lenders use it to assess the risk of lending you money. A higher score signals lower risk, translating to better interest rates, more favorable loan terms, and potentially lower down payment requirements.

Here's the credit score impact on interest rates and your wallet (in general terms):

- 760-850: The Gold Standard! Expect the lowest interest rates and the most attractive loan options.

- 700-759: Excellent! You'll still qualify for very competitive rates and favorable terms.

- 640-699: Good. You'll likely be approved, but interest rates will be slightly higher.

- 620-639: Acceptable. This range is often the minimum for conventional loans, but be prepared for less favorable rates.

As the guide shows, aiming for a 740+ score can lead to best rates and closing costs on mortgage loans, especially Conventional Mortgage Loans,.

.png "Minimum Credit Score Requirements for Kentucky Mortgage Loans")

Kentucky Mortgage Options: Credit Score Requirements Deconstructed.

Let's explore the minimum credit score requirements for different Kentucky mortgage types:

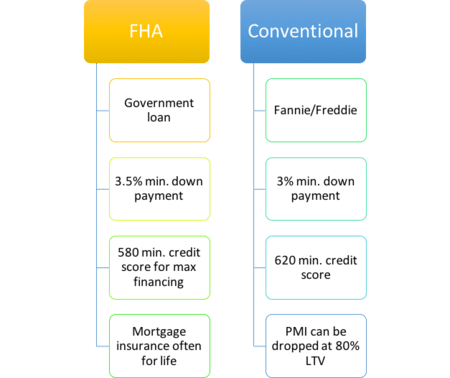

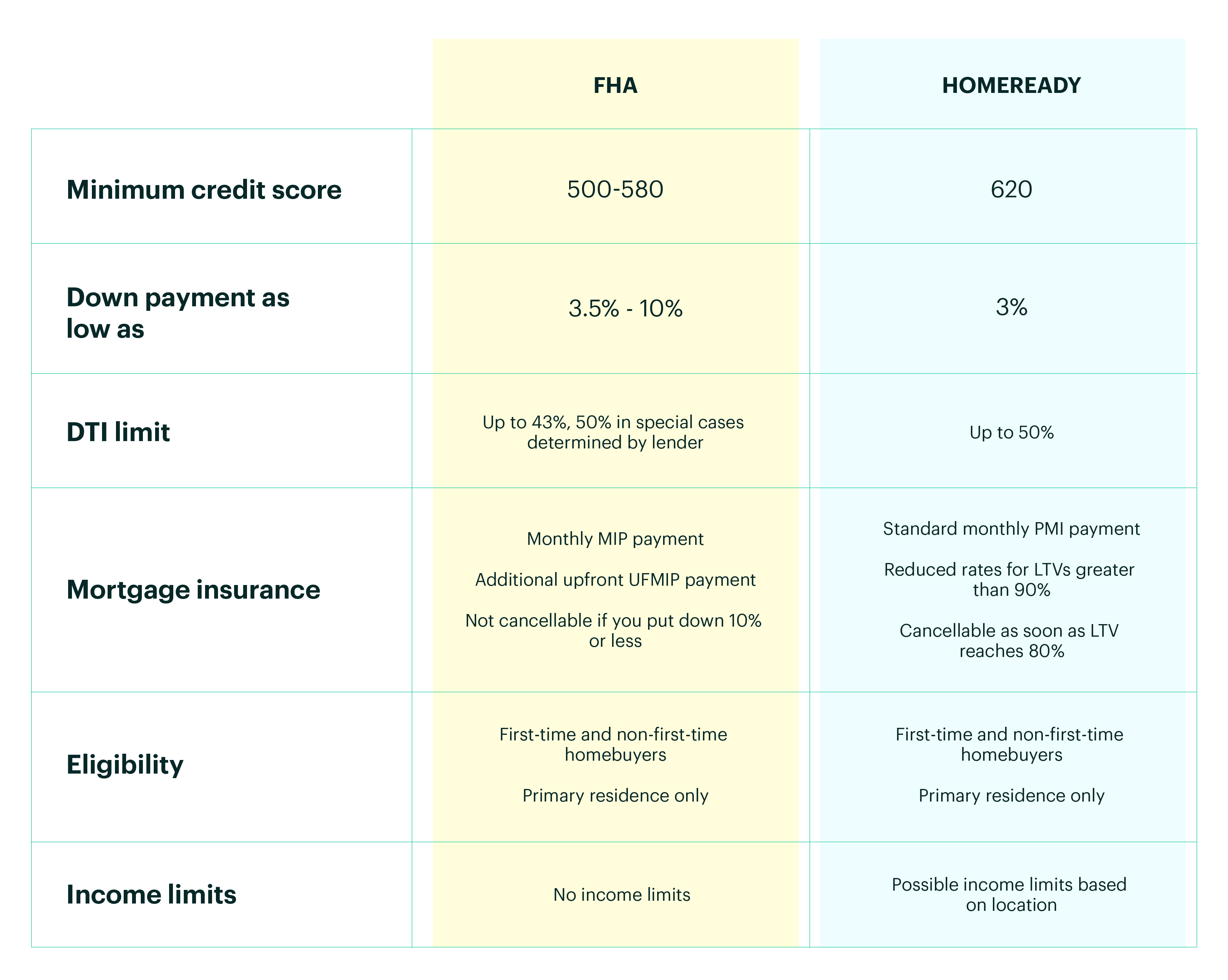

Conventional Loan

• At least 3%-5% down• Closing costs will vary on which rate you choose and the lender. Typically, the higher the rate, the lesser closing costs due to the lender giving you a lender credit back at closing for over par pricing. Also, called a no-closing costs option. You have to weigh the pros and cons to see if it makes sense to forgo the lower rate and lower monthly payment for the higher rate and less closing costs.

Fico scores needed start at 620, but most conventional lenders will want a higher score to qualify for the 3-5% minimum down payment requirements Most buyers using this loan have high credit scores (over 720) and at least 5% down.

The rates are a little higher compared to FHA, VA, or USDA loan but the mortgage insurance is not for life of loan and can be rolled off when you reach 80% equity position in home. Conventional loans require 4-7 years removed from Bankruptcy and foreclosure.

Kentucky USDA Rural Housing Program

If you meet income eligibility requirements and are looking to settle in a rural area, you might qualify for the KY USDA Rural Housing program. The program guarantees qualifying loans, reducing lenders’ risk and encouraging them to offer buyers 100% loans. That means Kentucky home buyers don’t have to put any money down, and even the “upfront fee” (a closing cost for this type of loan) can be rolled into the financing.

Fico scores usually wanted for this program center around 620 range, with most lenders wanting a 640 score so they can obtain an automated approval through GUS. GUS stands for the Guaranteed Underwriting system, and it will dictate your max loan pre-approval based on your income, credit scores, debt to income ratio and assets.

They also allow for a manual underwrite, which states that the max house payment ratios are set at 29% and 41% respectively of your income.

They loan requires no down payment, and the current mortgage insurance is 1% upfront, called a funding fee, and .35% annually for the monthly mi payment. Since they recently reduced their mi requirements, USDA is one of the best options out there for home buyers looking to buy in a rural area

A rural area typically will be any area outside the major cities of Louisville, Lexington, Paducah, Bowling Green, Richmond, Frankfort, and parts of Northern Kentucky. There is a map link below to see the qualifying areas.

There is also a max household income limits with most cutoff starting at 109,500 for a family of four, and up to $136,000 for a family of five or more.

The income limits change every spring, so make sure and check to see what updated income limits are.

USDA requires 3 years removed from bankruptcy and foreclosure

There is no max USDA loan limit.

Kentucky FHA Loan

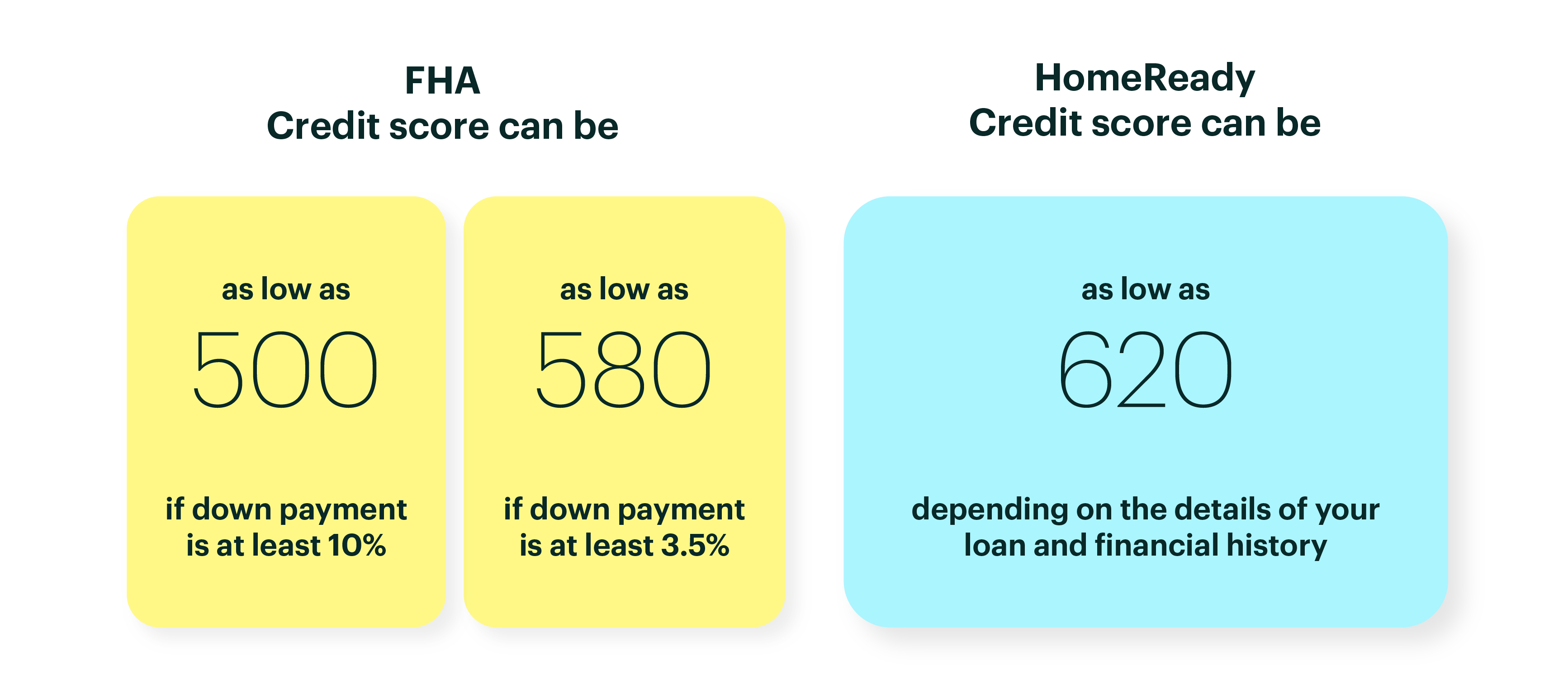

FHA loans are good for home buyers with lower credit scores and no much down, or with down payment assistance grants. FHA will allow for grants, gifts, for their 3.5% minimum investment and will go down to a 580-credit score.

The current mortgage insurance requirements are kind of steep when compared to USDA, VA, but the rates are usually good so it can counteract the high mi premiums. As I tell borrowers, you will not have the loan for 30 years, so don’t worry too much about the mi premiums.

The mi premiums are for life of loan like USDA.

FHA requires 2 years removed from bankruptcy and 3 years removed from foreclosure.

Kentucky VA Loan

VA loans are for veterans and active-duty military personnel. The loan requires no down payment and no monthly mi premiums, saving you on the monthly payment. It does have an funding fee like USDA, but it is higher starting at 2% for first time use, and 3% for second time use. The funding fee is financed into the loan, so it is not something you have to pay upfront out of pocket.

VA loans can be made anywhere, unlike the USDA restrictions, and there is no income household limit and no max loan limits in Kentucky

Most VA lenders I work with will want a 580-credit score, even though VA says in their guidelines there is no minimum score, good luck finding a lender

VA requires 2 years removed from bankruptcy or foreclosure

Clear Caviars needed to for a VA loan.

Kentucky Down Payment Assistance

This type of loan is administered by KHC in the state of Kentucky. They typically have $10,000 down payment assistance year around, that is in the form of a second mortgage that you pay back over 10 years. Current terms are $10,000 over 10 years at 3.75%

Sometimes they will come to market with other down payment assistance and lower market rates to benefit lower income households with not a lot of money for down payment.

KHC offers FHA, VA, USDA, and Conventional loans with their minimum credit scores being set at 620 for all programs. The conventional loan requirements at KHC requires 660 credit score.

The max debt to income ratios is set at 50% and 50% respectively.

FHA Loans – Best for First-Time Homebuyers with Low Credit

500-579 Credit Score – Requires 10% down payment

580+ Credit Score – Requires 3.5% down payment

Flexible credit guidelines & lower down payments

Easier approval for first-time buyers & those with past credit issues

VA Loans – Best for Veterans and Active Military

No official minimum credit score

Most lenders require 580-620+

0% down payment – No mortgage insurance required

Best for veterans, active-duty military & eligible spouses

USDA Loans – Best for Rural & Suburban Homebuyers

Minimum 620 to 640+ Credit Score (for automatic approval through GUS )

Some lenders may approve below 640 with manual underwriting with a minimum score of 581 and above

0% down payment required

Best for low-to-moderate-income homebuyers in rural areas Income limits and property locations restrictions

Conventional Loans – Best for Borrowers with Good Credit

Minimum 620+ Credit Score-Truthfully, if scores are 620 and less than 20% down payment look at going to the government loan programs like FHA, USDA and VA

Higher scores (760+) qualify for better interest rates

Down payment: 3%-5% or more

Best for buyers with strong credit & stable income

Kentucky Housing Corporation (KHC) Loans – First-Time Buyer Assistance

Minimum 620+ Credit Score, Income limits and max dti is 50% usually used for the down payment and closing costs on a FHA, VA, USDA or Conventional loan with the $10k DAP assistance

Offers down payment assistance for eligible buyers

Best for first-time homebuyers needing financial help

Non-QM Loans – Alternative Financing for Unique Situations

Minimum 500-620 Credit Score (Varies by lender)

Includes Bank Statement Loans, DSCR Loans, Asset-Based Loans

Best for self-employed borrowers, real estate investors & those with non-traditional income sources

Why Choose Non-QM? These non-traditional loans are great for borrowers who don’t qualify for conventional or government-backed loans due to income verification challenges.

How Credit Scores Affect Mortgage Interest Rates

Your credit score doesn’t just determine loan eligibility—it also affects the interest rate you receive.

Here’s how credit scores impact mortgage rates (examples based on typical loan rates):

| Credit Score | Estimated Interest Rate | Kentucky Mortgage Loan Options Available |

|---|---|---|

| 760-850 | Best Rate (Lowest Cost) | Kentucky Conventional, FHA, VA, USDA |

| 700-759 | Good Rate | Kentucky Conventional, FHA, VA, USDA |

| 640-699 | Higher Rate | Kentucky FHA, VA, USDA, Some Conventional |

| 620-639 | Even Higher Rate | Kentucky FHA, VA, USDA, Some Conventional |

| Below 620 | Limited Options, Highest Rates | FHA, VA, USDA and (with higher down payment), Non-QM |

Email - kentuckyloan@gmail.com

Email - kentuckyloan@gmail.com  Call/Text - 502-905-3708

Call/Text - 502-905-3708Joel Lobb

Mortgage Loan Officer - Expert on Kentucky Mortgage Loans

Website: www.mylouisvillekentuckymortgage.com

Website: www.mylouisvillekentuckymortgage.com Address: 911 Barret Ave., Louisville, KY 40204

Address: 911 Barret Ave., Louisville, KY 40204

Evo Mortgage

Company NMLS# 1738461

Personal NMLS# 57916

For assistance with Kentucky mortgage loans, reach out via email, call, or text Joel Lobb directly.

Kentucky Local Home Loan Lender Services

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process

First-Time Home Buyers Welcome FHA, Rural Housing (USDA), VA, and Kentucky Housing Corporation (KHC) Loans Conventional Loan Options Available Fast Local Decision-Making Experienced Guidance Through the Home Buying Process