Kentucky First-Time Homebuyer Loan Programs: FHA, VA, and USDA Explained

If you're a first-time homebuyer in Kentucky, navigating the mortgage landscape can feel overwhelming—but it doesn’t have to be. At Joel Lobb, Mortgage Loan Officer, we simplify the process by helping you understand your best loan options.

FHA Loan – Ideal for Buyers with Lower Credit Scores

Minimum Credit Score: 580+ (lower scores possible with a higher down payment)

Down Payment: 3.5% minimum

Debt-to-Income Ratio:

-

Front-End: Max 45%

Back-End: Max 56.99%

Employment: Steady job history (2 years preferred)

Past Credit Issues: Lenient with past bankruptcy or foreclosure

Time to Close: ~30–45 days

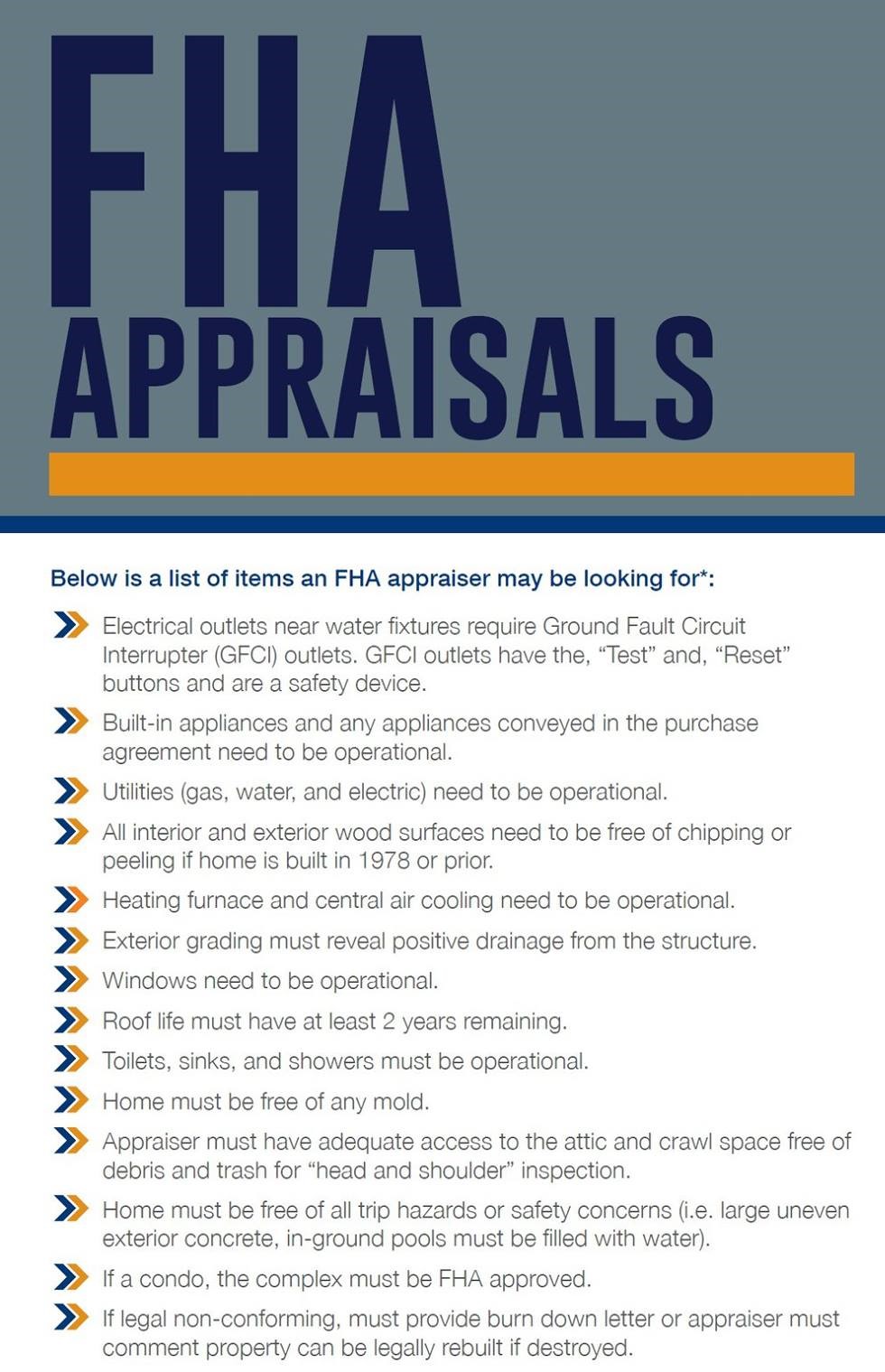

Appraisal Requirements: Must meet FHA’s Minimum Property Standards

Income Documentation:-

Recent pay stubs

-

W-2s (past 2 years)

-

Tax returns

-

Proof of any additional income

VA Loan – Zero Down for Veterans and Active Duty Military

- Minimum Credit Score: No official requirement (most lenders look for 620+)

- Down Payment: None required

- Debt-to-Income Ratio: 41% (can go higher with compensating factors' good residual income, high credit scores, lots of reserves and assets)Residual Income Requirements. Click here

- Employment: Stable income and employment for last two years

- Past Credit Issues: More flexible on bankruptcies and foreclosures

- Time to Close: ~45–60 days-

- Appraisal Requirements: Property must meet VA Minimum Property Requirements (MPRs)

- Income Documentation:

-

Pay stubs

-

W-2s

-

Tax returns

-

Documentation for bonuses, alimony, rental income (if applicable)

USDA Loan – No Money Down for Rural Kentucky Buyers

- Minimum Credit Score: 640 for GUS AUTOMATED APPROVAL (some exceptions possible on a manual underwrite with no score)

- Down Payment: 0%

- Debt-to-Income Ratio: 32%and 45% with 2 history (2 years preferred of work. Minimum of 12 months)

- Past Credit Issues: Consideration given to past credit challenges, bankruptcy, or foreclosure

- Time to Close: ~30–60 days-A little longer due to conditional commitment needed from USDA so a two step process to get final clear to close.

- Appraisal Requirements: Must pass USDA’s health and safety standards, typically must pass FHA HUD standards for appraisal requirements but does not have to be done by a FHA appraiser.

- Income Documentation:

-

Pay stubs

-

W-2s

-

Federal tax returns (last 2 years)

-

Documentation for other income streams

Appraisal requirements and income documentation

FHA Loan: Appraisal Requirements:

Income Documentation:

VA Loan: Appraisal Requirements:

Income Documentation:

USDA Loan: Appraisal Requirements:

Income Documentation:

These appraisal requirements and income documentation are crucial parts of the loan application process. Lenders use this information to assess the property's value, ensure it meets safety standards, and verify the borrower's income stability and ability to repay the loan.

Joel Lobb Mortgage Loan Officer

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

.jpg "Applies to case numbers assigned on or after June 1, 2022 Updates the initial appraisal validity period from 120 days to 180 days from the effective date of the appraisal report; Extends the appraisal update validity period from 240 days to one year from the effective date of the initial appraisal report; Allows the appraisal update to be ordered AFTER an appraisal expires; and Eliminates the optional 30-day extension. ✨This is big news for FHA ✨ The guideline change also puts FHA appraisal expirations on par with conventional loan expiration dates.")

{kind=link}