What are Kentucky VA Home Loans?

VA Loans provide military veterans and current service members a distinct advantage when it comes time to purchase or refinance a home. Today's VA Loans have the most favorable terms available for most veterans. VA Loans can be used to purchase a new home with no down payment with no mortgage insurance or refinance up to 90% of homes current equity.

What are the eligibility requirements for a VA Loan in Kentucky?

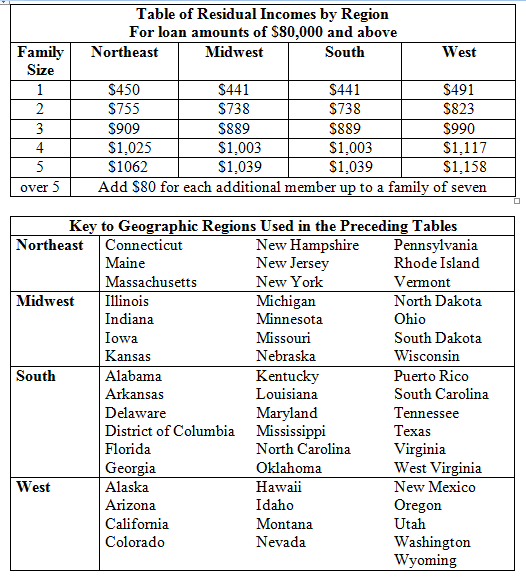

Veterans Affairs loan guidelines use two methods of income qualification in Kentucky. The residual income method is the primary method, where it is determined that the borrower has sufficient income to cover daily living costs once housing, taxes, insurance and all other liabilities like credit card and auto payments have been made. Additionally, VA loans use a debt to income ratio (DTI).

Using this ratio, the veteran's total debt should not exceed 41% of the veteran's total income. Most lenders will require at least a 580 to 620 credit score for a VA Loan approval. Keep in mind, VA guidelines do not call for a credit score but most lenders institute minimum credit score overlay to protect from buybacks from VA loans if they have too many go into foreclosure

The maximum Kentucky VA Mortgage amount is determined by:

Maximum VA Loan in Kentucky: The largest loan allowed for VA mortgages with zero down is now based on your VA loan entitlement in KY. Please refer to the Kentucky VA Loan Limit chart at the bottom of this page to see your area's limit.

Maximum Finance: For purchase transactions, the Maximum VA Loan will be 100% of the lower of the selling price or the appraised value.

No down payment required and closing costs vary from lender to lender and usually is based upon the loan amount, credit score, time to close (lock period) and whether or not you get a par rate or a higher rate with a lender credit to pay some of your closing costs at closing.

VA Loans may be used to purchase or refinance single-family residences and VA approved condo projects if the property is the veteran's primary residence.

Three kinds of VA Refinance programs are available for veterans in Kentucky.

Rate/Term VA Refinance

The Rate/Term VA Refinance can be used to refinance a conventional, FHA or subprime mortgage into a stable, fixed rate VA Loan.

VA Cash-Out Refinance

A Cash-Out VA Refinance is very beneficial for the veteran who wants to access the equity that they have built up in their home. VA Loans can be used to refinance up to 90% of a home's current value and take cash out for any reason.

Streamline Refinance

The VA Streamline Refinance is designed to lower the interest rate on a current VA mortgage or convert a current VA adjustable-rate mortgage into a fixed rate. A VA Streamline Refinance Loan can be performed quickly and easily. It requires much less hassle and paperwork than a normal refinance including no appraisal, no qualifying debt ratios and no income verification.

The maximum amount for an KY VA loan is determined by:

Maximum VA Loan in Kentucky: The largest loan allowed for a VA Mortgage varies from county to county. To see what the limit is in the county in which you're interested, visit the following page

👇👇

https://www.benefits.va.gov/HOMELOANS/purchaseco_loan_limits.asp.

This site lists U.S. territories as well as states.

Maximum Finance: In Kentucky, the maximum VA refinance loan amount will be 100% of the appraised value of the home for a rate/term refinance or 100% of the appraised value for a VA cash out refinance.

VA refinance loans use two methods for income qualification purposes in Kentucky. The residual income method is the primary method, where it is determined that the borrower has sufficient income to cover daily living costs once housing, taxes, insurance and all other liabilities like credit card and auto payments have been made. Additionally, VA loans use a debt-to-income ratio (DTI). Using this ratio, the veteran's total debt should not exceed 41% of the veteran's total income. Most lenders will require at least a 580-credit score for a VA Loan approval.

Kentucky VA Mortgages require no down payment.

There are no prepayment penalties for VA Home Loans.

A Kentucky VA Loan is fully assumable, provided the person assuming is qualified.

VA Mortgage Loans have no PMI premiums.

A VA Mortgage Loan is eligible for non-credit qualifying, Streamline Refinance or "IRRRL".

A VA Home Mortgage is available all areas of the country, provided a market exists for the property and the home meets VA's property standards.

A VA Home Loan may be used to purchase or refinance a new or existing home.

Kentucky VA Loans are offered at terms of 15 or 30 years.

How much can I borrow?

The maximum Kentucky VA Mortgage amount is determined by:

Maximum VA Loan in Kentucky: The largest loan allowed for VA mortgages with zero down is now based on your VA loan entitlement in KY. Please refer to the Kentucky VA Loan Limit chart at the bottom of this page to see your area's limit.

Maximum Finance: For purchase transactions, the Maximum VA Loan will be 100% of the lower of the selling price or the appraised value.

What will the down payment and closing costs be?

No down payment required and closing costs vary from lender to lender and usually is based upon the loan amount, credit score, time to close (lock period) and whether or not you get a par rate or a higher rate with a lender credit to pay some of your closing costs at closing.

What property types are allowed for VA Loans in Kentucky?

VA Loans may be used to purchase or refinance single-family residences and VA approved condo projects if the property is the veteran's primary residence.

Can I do a VA refinance in Kentucky?

Three kinds of VA Refinance programs are available for veterans in Kentucky.

Rate/Term VA Refinance

The Rate/Term VA Refinance can be used to refinance a conventional, FHA or subprime mortgage into a stable, fixed rate VA Loan.

VA Cash-Out Refinance

A Cash-Out VA Refinance is very beneficial for the veteran who wants to access the equity that they have built up in their home. VA Loans can be used to refinance up to 90% of a home's current value and take cash out for any reason.

Streamline Refinance

The VA Streamline Refinance is designed to lower the interest rate on a current VA mortgage or convert a current VA adjustable-rate mortgage into a fixed rate. A VA Streamline Refinance Loan can be performed quickly and easily. It requires much less hassle and paperwork than a normal refinance including no appraisal, no qualifying debt ratios and no income verification.

How much can I refinance in Kentucky?

The maximum amount for an KY VA loan is determined by:

Maximum VA Loan in Kentucky: The largest loan allowed for a VA Mortgage varies from county to county. To see what the limit is in the county in which you're interested, visit the following page

👇👇

https://www.benefits.va.gov/HOMELOANS/purchaseco_loan_limits.asp.

This site lists U.S. territories as well as states.

Maximum Finance: In Kentucky, the maximum VA refinance loan amount will be 100% of the appraised value of the home for a rate/term refinance or 100% of the appraised value for a VA cash out refinance.

What factors determine if I am eligible for a VA Refinance Loan?

VA refinance loans use two methods for income qualification purposes in Kentucky. The residual income method is the primary method, where it is determined that the borrower has sufficient income to cover daily living costs once housing, taxes, insurance and all other liabilities like credit card and auto payments have been made. Additionally, VA loans use a debt-to-income ratio (DTI). Using this ratio, the veteran's total debt should not exceed 41% of the veteran's total income. Most lenders will require at least a 580-credit score for a VA Loan approval.

Why choose a VA Home Loan?

Kentucky VA Mortgages require no down payment.

There are no prepayment penalties for VA Home Loans.

A Kentucky VA Loan is fully assumable, provided the person assuming is qualified.

VA Mortgage Loans have no PMI premiums.

A VA Mortgage Loan is eligible for non-credit qualifying, Streamline Refinance or "IRRRL".

A VA Home Mortgage is available all areas of the country, provided a market exists for the property and the home meets VA's property standards.

A VA Home Loan may be used to purchase or refinance a new or existing home.

Kentucky VA Loans are offered at terms of 15 or 30 years.

Joel Lobb

Senior Loan Officer

(NMLS#57916

text or call my phone: (502) 905-3708

email me at kentuckyloan@gmail.com

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people. NMLS ID# 57916,

(www.nmlsconsumeraccess.org). Mortgage loans only offered in Kentucky.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice. Manufactured and mobile homes are not eligible as collateral.

All loans and lines are subject to credit approval, verification, and collateral evaluation and are originated by lender. Products and interest rates are subject to change without notice. Manufactured and mobile homes are not eligible as collateral.